Part Two: Problems with Profits

I.C. Angles Investment Post

Record corporate profits are this stock market’s feet of clay. And it’s just a matter of time until they crumble. Although the rise in stock prices most recently has come largely from stocks simply becoming more expensive, as discussed in part one of “This isn’t Going to End Well” rising corporate earnings are also playing a critical role. Counter intuitively, there are two key reasons record profits are actually bad for future stock market prices. First, profits are mean reverting. History, teaches that record high profits, eventually fall and revert to their arithmetic mean over time–an action that takes stock prices lower in the process. Second, rather than strong economic growth and innovations around productivity driving profitability higher, profit growth has been increasingly generated by wage suppression and financial engineering.

At the mid point of 2014 earnings had increased by about 53 percent over the past four years, while stocks have increased 107 percent. In other words, as previously noted much of the rise in stock prices stem purely from stocks becoming more expensive. In fact since the Federal Reserve announced its Operation Twist in 2011, the pattern of stocks rising based on richer valuations, rather than profits has been most pronounced. Nevertheless, rising earnings have still played a key role in the continuing rise in stock prices. Although it appears that Fed efforts to push investors out on the risk curve have been successful at driving stock prices higher, than even rising corporate profits might warrant. But there is good reason to worry about profits, as well as valuations, based on history.

Revision to the Mean

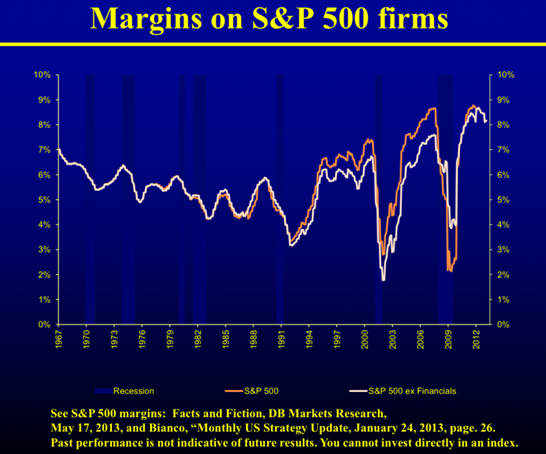

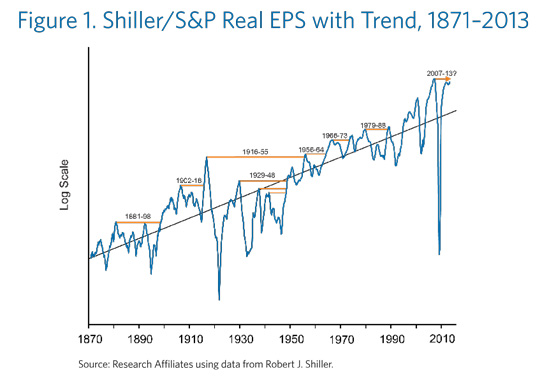

Profit margins may never have been higher, but they have certainly seen their highs and lows over time. The below chart courtesy of the Blackstone Group shows profit margins of S&P 500 companies going back to 1967. Typically and not surprisingly, profit margins tend to peak before recessions and then roll over. Current trends would also suggest when profits roll over, they will overshoot their median, as recent cycles have become more extreme. There is nothing in economic history to suggest profits can stay at a permanently high plateau, even if current rich stock valuations are embedding an expectation of profits rising even further. Looking at an even longer time period is also instructive. The accompanying chart courtesy of Research Associates presents earnings per share data back to 1871. Not only do periods of high earnings lead to reversals, but they have sometimes led to multi-decade periods of flat or negative real earnings per share growth. Something that is a distinct and very bearish possibility for the stock market. Last in this particular series I have included another way to look at profits, as a percentage of GDP contrasted also with recessions and the S&P 500 stock index.

Problems with Wage Suppression

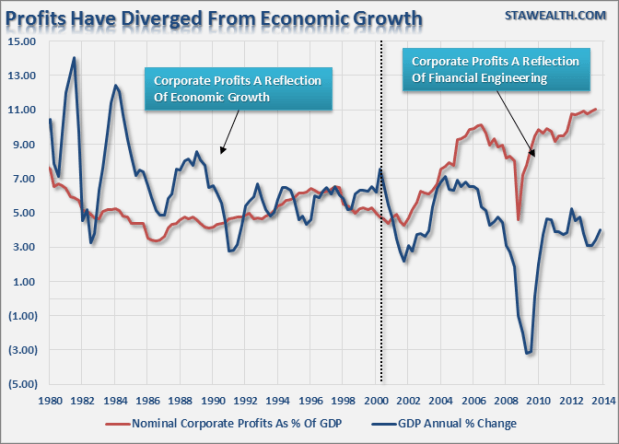

Revision to the mean isn’t the only problem for profits. Increasingly earnings are divorced from economic growth, while wage suppression is playing an important role, as the below charts from STA Wealth management illustrate. But there are two significant problems with this paradigm. Holding down worker’s compensation to increase profits means less future sales and revenue growth from companies, as consumers have less money to pay for goods and services. Today’s consumers appear close to fully leveraged in terms of using more debt to pay for greater consumption, so wage growth is badly needed to drive robust economic growth that has been largely absent since the last recession. Alternatively, wage suppression means a less robust economy, and likely a more severe future recession with ultimately lower corporate profits. In addition, wage suppression increases the odds of political upheaval or legislative redress in those countries corporations operate within, which would likely negatively impact corporate profitability.

Problems with Financial Engineering

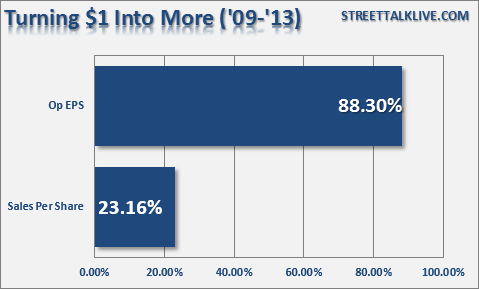

Along with wage suppression, financial engineering has also played a major role in elevating corporate profits. And it also has significant negative implications for stock investors. The below bar chart courtesy of STA Wealth Management compares the growth in operating earnings per share of S&P 500 companies of over 88 percent versus sales growth of over 23 percent from January 2009 to December 2013. The difference between the two numbers is largely financial engineering or as some might call them accounting tricks, e.g. amortization, one-time write offs, depreciation and stock buybacks. But there are limits to pushing earnings higher through financial engineering, rather than actual sales growth, and there are also consequences, particularly in the case of share buybacks.

Buying Earnings with Debt

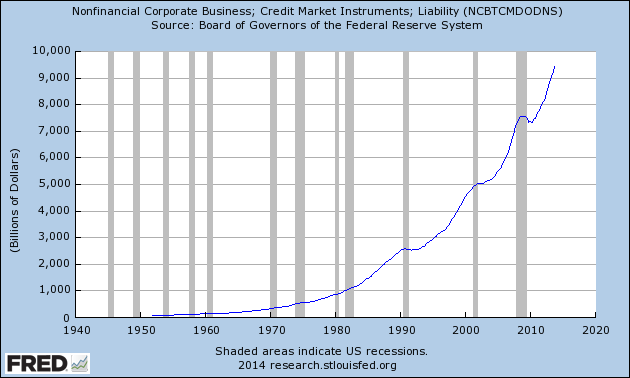

Corporations buying back their own shares, reduce the number of shares, thereby driving up the earnings per share without the need to actually earn any more money. With easy access to credit, and thanks to the Federal Reserve historically low interest rates, this has been a strategy many corporations have adopted. As a result, corporations have been some of the most active buyers of stocks in the market most recently. They have not only pushed EPS higher, but also helped drive the stock market higher. But, as with all things, there is a catch. Buying stock at higher and higher prices, likely represents a bad deal for shareholders and it comes at the price of rising levels of corporate debt and increasingly unhealthy balance sheets. While corporate debt peaked in the 2009 recession at $7.3 trillion, five years later it had grown to well over $9.6 trillion. Despite all the talk about corporations holding immense amounts of cash, thanks largely to share buybacks their cash holding relative to corporate debt is at the lowest level in fifteen years, as can be seen in the below chart courtesy of Deutsche Bank. In addition, there is a limit to how long corporations can stay on a path of increasing buybacks via debt.

The Bottom Line on Profits

The Fed’s extreme monetary policy has not delivered a healthy economy, with strong employment and income growth. But it has delivered healthy corporate profits, an over-priced stock market and record levels of absolute corporate debt. Unfortunately, both the historical pattern of profitability and the nature of how corporations are generating profits, represent significant risks to stock market investors. There is no reason to think that currently elevated profit levels represent a sustainable and positive new economic paradigm. Instead there is every reason to believe profits will revert to their historical mean. Based on currently elevated earnings levels and profit strategies centered around wage suppression and financial engineering, the reckoning is likely to be particularly painful for stock investors. The peaking of corporate profits prior to the next bear market for stocks is simply a matter of time.

This Isn’t Going to End Well–Part One: Stocks are too Expensive