I.C. Angles Investment Post…

As the stock market makes new highs, there are many reasons to worry that the fall could be particularly hard when it comes. I’m no permabear and have not been constantly arguing a bear market is around the corner. Even if I haven’t been the biggest cheerleader of stocks I have been an advocate. For example in August of 2011 I wrote about how, despite negatives, stocks were the best investment options available to most and in my February post this year I argued that despite rising risks investors should continue to hold stocks and a decline was unlikely to transpire until 2014. At the same time, starting in May of this year, as the stock market kept making new highs, I began to argue that risks in 2013 were rising and investors should use the strength to raise cash levels and sell some stocks, particularly money involving a low risk threshold and time horizon. As I look at where the stock market stands at the end of the year, I continue to believe the risks of a bear market being sooner rather than later have only grown.

Bear Checklist

In calling a bear market several factors should be considered, and not all of them are yet bearish. Key positive factors include technical indicators and economic fundamentals. On the other hand, I tend to believe valuations represent more a negative than a positive, and think John Hussman’s most recent analysis on the topic of valuations is worth consideration, even if he has fallen in the camp of being overly pessimistic and wrong on stocks over the years. What is not debatable is that this year’s stock rally has been characterized by expanding multiples and stocks becoming more expensive to a much greater extent than any improvement in corporate performance. In my view clear stock market negatives include: historical precedent, investor sentiment and systemic risks.

The Positives

At the most basic level, market technicals remain positive, with the stock market still on a path of making higher highs and higher lows. Nor have I seen any other major technical indicators that appear overly bearish. The biggest technical negatives may be in the charts of other countries. I have written about the stock market risks around a hard economic landing in China, and charts for stocks in China, Taiwan, South Korea, and particularly Australia are less bullish. The 1929 stock market crash was preceded by deterioration in foreign markets and it is worthwhile to keep an eye out for not just negative technicals in the U.S., but also overseas markets. It is also worth remembering just how swift a decline in the stock market could occur and technical indicators change, as the stock market rally topping in 1929 that ended in disaster is eerily similar to the current market rally. This should be considered less a prediction, than a warning from history of how fast stock market price action can go from very bullish to extremely bearish.

The stock market tends to lead the economy. So I consider economic performance largely a trailing indicator and among the least important factors to consider in analyzing the market. Nevertheless, recent U.S. economic performance has been more bullish than bearish. The Bureau of Economic Analysis recently reported that the U.S. economy grew at an annualized rate of 4.1 percent in the third quarter. The most recent U.S. employment report was also relatively strong with the unemployment rate falling to 7.0 percent. Both reports came with some important caveats, including that a significant portion of economic growth came from increasing inventory levels that were not offset by sales and will be a drag on future growth. Europe also has shown signs of stabilization and some strength, as well as Japan.

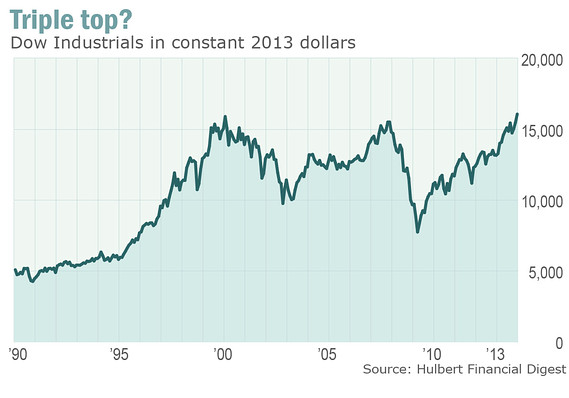

The Negatives

In terms of historical precedent I have written extensively of why I believe we are still in a secular bear market. I continue to hold to my belief we have at least one more major market downturn ahead, and the stock market is unlikely to make meaningful record highs or not revisit near or below previous bottoms. Secular bear markets have lasted significantly more, not less, than a decade. History would argue against the current stock market being able to sustain the move that began in 2009, above the 2000 top. The below chart shows that on an inflation-adjusted basis the stock market is only now currently challenging previous highs. I do think secular bear markets are best compared historically to one another on an inflation-adjusted basis, but I also believe that in hindsight no such adjustment will be needed to see the absence of a sustained breakout indicative of a secular bull starting.

Turning to sentiment, the Investors Intelligence Advisor Sentiment survey is showing levels of bullishness not seen since 1987 and exceeding the 2007 market top. Other sentiment indicators also show investors have become very confident in the stock market. Investors are putting the most money into stocks since 2000. Unfortunately, history demonstrates that stock market tops are correlated to extremely positive sentiment. There are already signs investors may have gotten ahead of themselves, as Thomson Reuters reported the most negative earnings guidance for Q4 in its history, with far more companies lowering guidance for their expected results than raising guidance. In fact the ratio of negative to positive is running at 10-1. Investors were wrong in 1987 when they believed portfolio insurance products had removed market risk, in 2000 when they thought Internet innovation had removed risks of economic downturns, and in 2007 when they were confident real estate was creating so much wealth as to remove the risks of a downturn and derivative products could eliminate systemic risks. I fully expect confidence that Federal Reserve policies can remove the risks around an economic or stock downturn, will prove just as misplaced.

A Split Verdict

In my view the risks of a systemic shock sending the stock market into a steep decline are far higher than investors appreciate. To name a few issues the potential for violent crisis in the world has not lessened, the underlying structural problems in the European monetary union not addressed, nor China proven to have engineered a soft economic landing. Extreme monetary policy also represents more a threat to than a source of stability. Quantitative easing in the U.S. has increasingly become a detriment to the economy on balance and unwinding it likely to be more destabilizing than currently believed. QE is the market equivalent of heroine to a drug addict—a Catch-22 where it is both damaging to keep consuming and, with the host dependent, dangerous to cease consuming.

But rather than having a fear of heights, investors are chasing strong stock market returns irrationally believing new highs represent safety from risk. Yet, I am unnerved by the similarities to how investors are currently looking at the Fed, as insuring against downturn risk in a manner in some psychological ways similar to portfolio insurance in 1987 or derivative products for the credit markets in 2007. Despite the selloff protections put in place since 1987, I am concerned about how steep a market sell off could be due to several factors. For one there is presently a lot of hot money in the stock market. Those who have jumped into the stock market chasing gains can just as quickly sell their stocks. In addition there are record levels of margin debt, and in the event of a decline those investors could be forced to sell stocks bought on borrowed money. We also don’t know how a market with a substantial amount of its volume represented by high frequency trading will act in a bear market, but that’s unlikely to be a source of stability.

It is for all the above reasons that starting this year I have become increasingly bearish, while still remaining a very reluctant bull on the stock market—unwilling to call a bear market, but advising selling some stocks into strength and raising cash. My current outlook remains to treat a significant sell off that breaks meaningful technical levels, as not a buying opportunity, but the moment to adopt a comprehensively defensive portfolio strategy. And I view the risks of a very steep decline high enough to warrant holding a meaningful cash position, along with long-term stock investments, even before such levels are breached.