I.C. Angles Investment Post

“Be fearful when others are greedy, and greedy when others are fearful.” – Warren Buffett, legendary investor

Recent volatility in the stock market has served as a barometer of investor sentiment and in my analysis only further confirms my recent market call, that regardless of near term price action, long-term investors should now be fearful of stocks. Most investors far too often end up buying high, selling low and realizing disappointing returns. A case in point is the current bull market that began in 2009. For the first few years, when prices were considerably lower, investors were much more fearful than now and inclined to sell or shun stocks. Of course that is what makes for a stock market bottom and the start of a new bull market–the investment herd selling their stocks, when things are at their worst. And the financial media only serves to exacerbate matters. Pushing stories of risks around depressions, financial calamity and double-dip recessions, when the market was bottoming. But that was actually the best time to be greedy. Now prices are much higher. And the investment herd is greedy to get a piece of stock market gains, while the financial media is favoring stories about how pull backs are buying opportunities. In my opinion, now is the time to be fearful and instead use rallies as selling opportunities… that is if you’re goal is to go contrary to the herd by buying low and selling high.

Reason to Fear in the Precedents

Both this bull market and economic recovery are beyond the average respective duration, and that should be reason for worry. This is an old bull market that based on history is far more likely to be near its end than its beginning. Other historical comparisons also give reason to worry. The below chart courtesy of Doug Short shows bad-bear-to-bull market cycles (Crash of 1929, 1973 oil embargo, 2000 Tech Crisis and the 2007 Financial Crisis). These comparisons show that such bad-bear-to-bull cycles have a long duration that typically runs for very similar time periods, and would imply a market top within a few more months. Then again, maybe this bad-bear-to-bull cycle will run longer than the others. And maybe this market will run far longer than the average, on the order of the 1990-2000 bull market. Maybe one of the weakest economic recoveries of the last century will generate one of the strongest, longest bull markets ever. But the level of confidence being exhibited from investors, currently holding and buying stocks at these levels, in such an optimistic outcome, seems misplaced at best.

Source: Dshort.com

Lack of Fear is a Sign of a Top

After stocks steadily climbing for over five years, there is good reason to now be getting fearful instead of greedy, when you look at historical precedent, as well as underlying fundamentals. Instead, current popular opinion seems to now treat any sell off as a buying opportunity. As stocks sold off recently there were few worries expressed of a market top. Instead, the consensus seemed to be to urge investors not to panic and to hold onto stocks, if not to buy more on the dips. This is in stark contrast to the early years of this bull market, where the fear of a double dip recession seemed omnipresent. There are many examples of this change in sentiment, but one of my favorites to illustrate just how far away we have moved from fear to greed is this recent Bloomberg article “Why the Stock Market Rally is Bad News,” detailing how the recent rally in stock prices after the sell off is bad news, because the selling didn’t last long enough for more investors to buy stocks, before the market returns to its inexorable rise. There just doesn’t seem to be a lot of fear or panic, and that is actually bad news for those holding stocks.

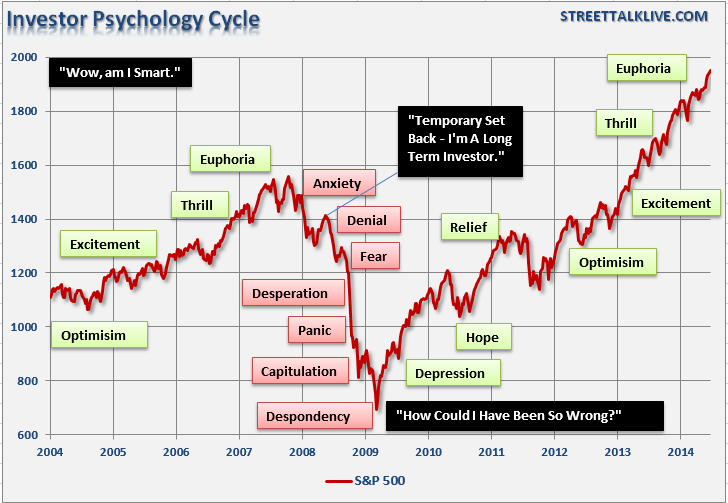

Just as market bottoms are created by the panic of investors pushing stocks down in their rush to get out at any price, market tops are created in the optimism that the market will keep rising and if investors don’t buy at current prices they will miss out on the next leg up. At the bottom, investors fear falling prices, and after selling stocks, they then have cash to buy stocks in the future and fuel the next rising bull market. Conversely, at the top, investors are greedy to profit from rising prices. Lance Roberts at Streettalklive.com created the below chart that illustrates the change in psychology investors experience, as stocks keep marching higher and they become increasingly more optimistic. Then, when stocks roll over and begin falling, psychology eventually shifts from optimism to growing pessimism, before the cycle starts all over again. However, in reference to the below chart, I might argue that rather than euphoria, recently investors have been exhibiting more a form of extreme complacency, believing there is little risk of losing money because central bankers, whether the U.S. Fed, ECB or Bank of Japan, will keep driving the stock market higher. Either way, the investment herd is feeling greedy, and rather than “panicking” in reaction to big sell offs, is looking to buy the dips. Such is the psychology of market tops that, whether the emotion is euphoria or extreme complacency, investors are far more greedy than fearful.

Source: Streettalklive.com

“Ill-timed Greed” is the Deadliest Sin

Bull markets end in greed. They die as the herd goes all in, and by committing so much of their available capital to stocks is no longer a potential source of more buying. Since investors have already bought, they are transformed into a future source of selling. Simply put, investors can’t buy stocks they already own, but they can sell them. And they certainly can’t buy stocks they’ve already borrowed for to buy on margin. My read of current sentiment indicates that the investment herd is in the last phases of their buying, indicative of a market top. Back in 2000 when I expressed worries of a market bubble around tech stocks, people would look at me like I was clueless. Then in 2007, when I worried about a real estate bubble, I got those same looks. Now I am again getting similar looks, as if I am clueless, for being fearful of a global monetary bubble popping and this bull market being close to its end. Ironically, the factor above all others that would make me reconsider my bearish call on the current market, as it makes new highs, would be if I had more company in my outlook. If this last sell off had indeed quickly produced the kind of panic that would indicate psychology had further to improve and people likely to commit more capital to stocks as it ran higher. Instead, people are increasingly fearless and greedy. That is exactly what market history teaches we should see around a top.