Part Four: Take the Money and Run

I.C. Angles Investment Post

“You’ve got to know when to hold ‘em. Know when to fold ‘em. Know when to walk away. Know when to run.” — Kenny Rogers, country music singer

“Go on take the money and run.” — The Steve Miller Band, American rock band

Risks around stocks have risen considerably, and even long term investors should now substantially underweight equity exposure. Due to the unique characteristics of this stock market, my best advice is to now treat it as if in the onset of a bear market, regardless of near term price action. At this point in 2014 many warning signs are flashing red—the bond market is signaling weakening growth and greater risk of default, while stock market breadth has deteriorated with many stocks, including small cap and foreign indices, exhibiting extended weakness, while fewer, very large stocks were supporting the market until the recent sell off. The risk versus reward of stock exposure has become too high for an even normal stock allocation, let alone the aggressive allocation most currently posses. It’s time to under weight stocks by taking money out of the market or hedging equity exposure with relation to key technical levels.

Time to Run or Hedge

Although there will likely be more warning before stocks decline in true bear market proportions and the market could very well rally higher from here, there is a very real risk of a market crash. For almost two years, coinciding with the Federal Reserve announcing its third round of quantitative easing nicknamed “QE Infinity”, every time the market has declined to its 125-day moving average enough buying support has come in to move stocks higher. That bullish pattern ended last week, as illustrated in the below chart. However, even if this is the initial stage of a bear market we should be able to assess more data before making that determination, since markets don’t tend to fall straight down. On the other hand, in 1987, as soon as the stock market penetrated its 200-day moving average, just above which the market closed on Friday, it collapsed. Furthermore, a big decline in stock prices below these levels is simply a matter of when in my view, as covered in Parts One, Two and Three, which explored how stocks are overpriced, record profits are likely to reverse and the nature of much economic growth in the current cycle is malignant. For all these reasons embracing defensive measures now makes good sense.

Source: BigCharts.com

History tends to rhyme more than repeat, and a replay of 1987 would seem unlikely. Then again, the market psychology of participants believing they are insured against risk, then through option products and now by the Federal Reserve’s QE policy, is very similar. In addition, given the backdrop of opaque financial arrangements and high derivative use in the global system, as well as immense amounts of hot money in this market, the risk of a crash is too real to ignore. Hot money includes the phenomena of high frequency trading, with the risk of a down move in the market being accelerated by computer program selling. Investors have also become more skittish, with retail investors in 2014 moving into stocks, but doing so by moving away from long-term equity mutual funds and buying ETF funds that can be more easily sold. Most worrisome from the perspective of the health of the stock market is record margin debt, as investors borrow to buy stocks. Margin debt peaked before the last two bear markets, and regardless of whether it has peaked again, it is at a worrisome high level, as seen below.

Source: dshort.com

Too Much Downside Risk

The risks of owning an even neutral weighting of stocks has become too high. My first post in this series detailed how stocks are too expensive. Stocks are pricing in continually rising corporate profits, but in my second post I explained why those hopes are likely to be dashed. On the other hand, stocks are not pricing in the global economic risks around China’s real estate bubble collapsing, further turmoil around a still structurally unsound European economic system, the apparent failure of Japan’s own quantitative easing policy, wars, disease, and the very real possibility that the Fed recognizing the failures of its own QE policy to generate broad-based economic growth, as covered in my third post of this series, but myopically concentrating on U.S. economic data, will not head off a market decline through liquidity injections.

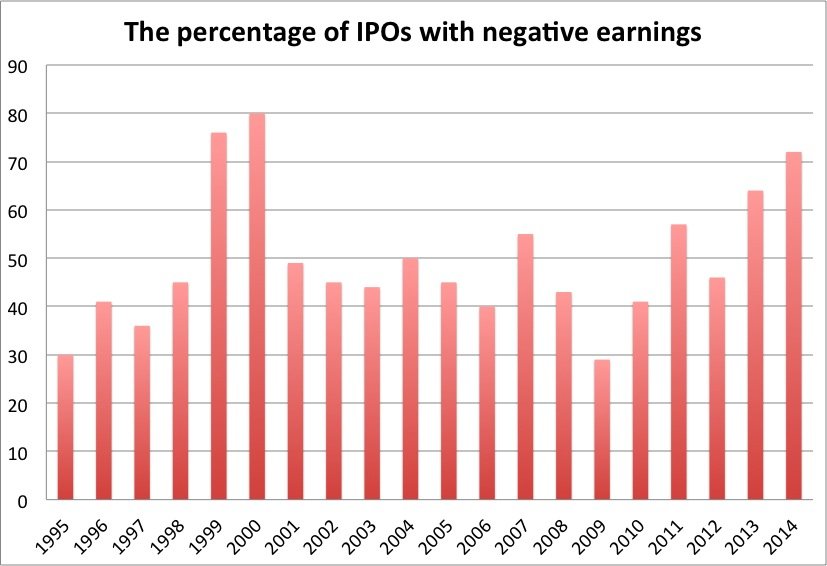

Contrarians may debate, whether current complacency is insufficient and investors need to become more bullish on stocks before a market top is likely. But in my estimation there is plenty of reason to worry that investors are about as heavily allocated, as they are going to be to stocks after the memory of the last two bear markets, before they become a source of selling pressure, rather than buying support. The latest data from the American Association of Individual Investors (AAII) showed bullish and bearish sentiment around average levels, but stock allocations above their historical average at 67 percent and around the levels achieved in the 2007 market top. Buying interest in the stock market for new companies that aren’t making any money at percentage (not aggregate) levels last seen in 2000 is one more sign investors are overlooking risks in a manner seen at market tops. Along similar lines, the ratio of buys to sells of stocks by corporate insiders is near the lowest level since the 2000 market top, indicating those with the best knowledge of their companies (the smart money) are increasingly negative on future prospects.

Source: Business Insider

How it Ends

This bull market will not last forever and at about five and a half years, is already well past the average of 3.8 years. Several characteristics of this stock market make me very nervous. Beyond some parallels to 1987, I am most worried about the similarities to 1929 and 1937, where subsequent losses were particularly painful. In 1929, the U.S. market crash was foreshadowed by deterioration in foreign stock markets, due to structural debt issues that would ultimately drive a deep global recession from which the U.S. could not decouple. In 1937, expansion in the monetary base, proved unable to sustain an economic and stock market breakout from the secular bear market of the Great Depression. Given the characteristics of today’s market, I fear the light so many see at the end of this tunnel will turn out to be an oncoming train.

In conclusion of my This Isn’t Going to End Well series, the risks around owning stocks have simply become too high in my opinion to justify the allocation an investor would typically employ in their investment portfolio. My view is that buying and holding stocks at present levels represents more potential risk than rewards, and those risks now warrant being very proactive in regards to protecting against downside losses. A substantial decline may or may not be imminent, but the risks discussed here of a steep fall, and the risks around valuations, profits and the character of growth, discussed in the first three parts, argue for even long-term buy-and-hold investors to reduce their equity exposure to below normal levels if they have not already and wait to rebuild equity positions when much better prices present themselves.

This Isn’t Going to End Well–Part One: Stocks are too Expensive

This Isn’t Going to End Well-Part Two: Problems with Profits

This Isn’t Going to End Well-Part Three: Malignant Growth

One comment